Most Indian car owners overpay for car insurance without realising it. Real-life stories, myths vs reality, mistakes to avoid, comparison table, FAQs, and smart tips to save thousands legally.

Why Most People Overpay for Car Insurance

(And Don’t Even Know They’re Doing It)

Car insurance is one of those things Indians buy once a year and forget.

No excitement.

No comparison.

No second thought.

And that’s exactly why most people overpay for car insurance every single year.

Not by ₹500.

Sometimes by ₹5,000–₹15,000 annually.

Multiply that over 5–7 years, and the loss becomes painful.

This article explains why it happens—and how to stop it without risking claims or legality.

The Biggest Misunderstanding About Car Insurance

Most people think:

“Insurance is fixed. Jo likha hai, wahi dena padega.”

That’s false.

In reality, car insurance pricing depends on:

- Your awareness

- Your questions

- Your willingness to say “no”

Insurance companies don’t cheat you.

Ignorance does.

Real-Life Story #1: Same Car, ₹9,200 Difference

Rahul and his neighbour both owned the same car model, same year.

At renewal time:

- Rahul paid ₹24,800 (dealer insurance)

- Neighbour paid ₹15,600 (online comparison)

Coverage? Almost identical.

Rahul’s reaction:

“Mujhe laga insurance toh insurance hoti hai.”

That assumption cost him ₹9,200.

Reason #1: Blindly Accepting Dealer Insurance

This is the number one reason people overpay.

Why Dealers Push Their Insurance:

- Higher commission

- One-click convenience

- Fear-based selling (“Claim mein problem hogi”)

Reality:

- Dealer insurance is usually the most expensive

- Claims don’t get rejected just because insurance is bought online

- Coverage can be equal or better outside

👉 Related read:

Save Money on Car Insurance – Complete Indian Guide

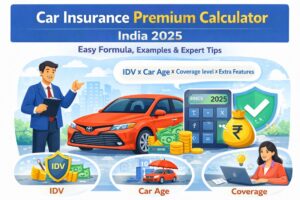

Reason #2: Not Understanding What You’re Paying For

Many owners don’t know:

- What IDV means

- What add-ons actually do

- What is mandatory vs optional

So they end up paying for:

- Add-ons they don’t need

- Inflated IDV

- Duplicate coverages

👉 Learn basics here:

How Car Insurance Works in India – Simple Guide

Comparison Table: Overpaying vs Smart Insurance Buyer

| Factor | Overpaying Buyer | Smart Buyer |

|---|---|---|

| Purchase method | Dealer | Online comparison |

| IDV selection | Maximum | Optimised |

| Add-ons | All selected | Only needed |

| No Claim Bonus | Ignored | Fully used |

| Renewal habit | Last-day panic | Planned |

| Annual premium | High | Optimised |

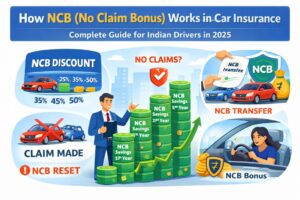

Reason #3: Ignoring No Claim Bonus (NCB)

NCB is free money most people waste.

Common Mistakes:

- Claiming small repairs

- Not transferring NCB to new car

- Not checking NCB percentage

NCB can reduce premium by up to 50% over time.

👉 Must-read:

How No Claim Bonus Works in Car Insurance

Real-Life Story #2: The ₹7,000 Claim That Cost ₹40,000

Sunita from Surat made a ₹7,000 insurance claim for a bumper scratch.

Result:

- Lost accumulated NCB

- Paid higher premium for next 3 years

Total loss over time: ₹40,000+

Her regret:

“Claim karna free laga, par mehenga pad gaya.”

Reason #4: Paying for Add-ons You Don’t Need

Add-ons are useful—but only if they match your usage.

Commonly Overused Add-ons:

- Engine protect (for dry cities)

- Consumables cover (low value)

- Key loss (rare usage)

- Invoice cover for old cars

Add-ons are not bad.

Blind add-ons are.

👉 Helpful breakdown:

Types of Car Insurance Explained

Reason #5: Overvaluing IDV “For Safety”

Indian mindset:

“IDV zyada rakhenge toh claim zyada milega.”

Reality:

- Higher IDV = higher premium

- Claim payout depends on depreciation and damage

- Inflated IDV mostly benefits insurer

Correct IDV = market value, not emotional value.

👉 Deep dive:

What Is IDV in Car Insurance & How to Calculate It

Reason #6: Fear That Online Insurance Means Claim Trouble

This fear is outdated.

Truth:

- Claims are handled by insurer, not agent

- Cashless garages are available nationwide

- Digital claims are faster in many cases

You’re not safer because you paid more.

You’re safer because you chose the right coverage.

Myth vs Reality: Car Insurance Edition

| Myth | Reality |

|---|---|

| Dealer insurance is safest | It’s just costliest |

| Higher premium = better claim | Coverage matters |

| Small claims don’t hurt | They kill NCB |

| Online insurance is risky | It’s regulated |

| Add-ons are compulsory | Most are optional |

Mistakes That Make You Overpay Every Year

❌ Renewing at last moment

❌ Not comparing quotes

❌ Claiming minor repairs

❌ Accepting dealer fear tactics

❌ Not checking IDV

❌ Forgetting NCB

These mistakes don’t feel expensive instantly.

They drain money slowly, yearly.

Editor’s Pick: How Smart Indians Save on Insurance

- Compare quotes annually

- Optimise IDV, don’t max it

- Protect NCB seriously

- Choose add-ons based on usage

- Renew before expiry

- Avoid small claims

- Read policy summary once

This alone can save ₹10,000–₹20,000 over ownership.

FAQs (What Car Owners Actually Ask)

1. Is cheapest insurance always best?

No. Cheapest with correct coverage is best.

2. Can I buy insurance without dealer?

Yes, completely legal and common.

3. Should I claim for small scratches?

Usually no. Pay from pocket if amount is small.

4. Is zero depreciation worth it?

Yes, especially for new cars and beginners.

5. Does insurance price reduce as car ages?

Yes, if you optimise IDV and keep NCB.

6. Can I switch insurer every year?

Yes, without losing NCB.

7. What’s the biggest overpayment reason?

Fear-based buying without comparison.

Final Truth: Insurance Is Boring—But Ignoring It Is Expensive

Car insurance won’t excite you.

But overpaying for it will definitely hurt later.

Most people don’t overpay because they’re careless.

They overpay because nobody explained it properly.

Now you know.

Strong CTA 🚗💰

👉 Bookmark this article before renewal

👉 Share it with someone renewing insurance soon

👉 Explore more honest, India-first car finance guides on Car Insight Hub

Because saving money on insurance doesn’t mean cutting corners—

it means cutting ignorance.

Disclaimer: This article is published for general informational purposes based on research, observations, and owner experiences. It should not be considered professional, technical, or legal advice. Vehicle specifications, costs, and procedures may vary by model, location, and time. Readers are advised to verify details with official sources or qualified professionals before making decisions.