Confused about car insurance types? This complete Indian guide explains third-party, comprehensive, add-ons, myths, mistakes, FAQs, and how to choose the right car insurance without overpaying.

Types of Car Insurance – Complete Guide for Indian Car Owners

Car insurance is mandatory in India.

But understanding car insurance? That’s optional—and most people skip it.

The result?

- Overpaying every year

- Wrong coverage

- Claim disappointments

- Fear-based buying

This guide is written to explain car insurance clearly, in simple Indian context, without jargon or sales pressure.

If you understand this once, you’ll never be confused again.

Why Understanding Car Insurance Matters More Than You Think

Most people treat car insurance like:

“Bas renew kar do, jo bhi ho.”

But car insurance affects:

- Your legal safety

- Your financial risk

- Your peace of mind after accidents

Choosing the wrong type of insurance doesn’t show immediately—but it hurts when something goes wrong.

What Is Car Insurance (In Simple Words)?

Car insurance is a contract where:

- You pay a premium

- The insurance company covers financial losses from:

- Accidents

- Theft

- Natural disasters

- Third-party damage

In India, at least third-party insurance is legally compulsory.

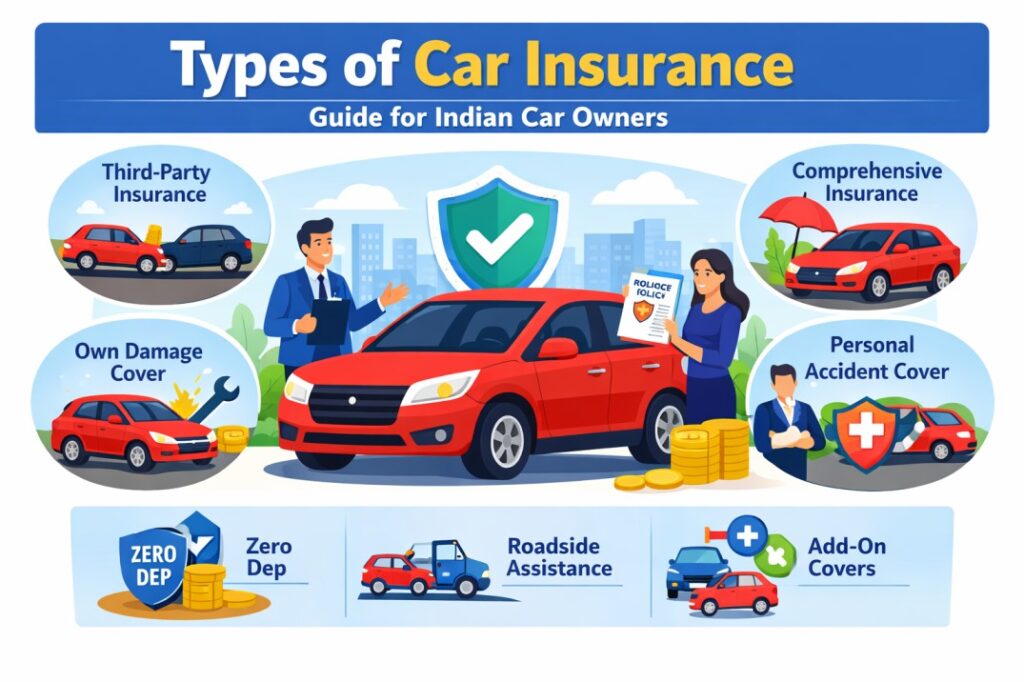

Main Types of Car Insurance in India

There are three primary categories every car owner must understand:

- Third-Party Car Insurance

- Comprehensive Car Insurance

- Standalone Own-Damage Insurance

Let’s break them down simply.

1. Third-Party Car Insurance

What It Is

Third-party insurance covers:

- Injury or death of another person

- Damage to someone else’s vehicle or property

It does not cover damage to your own car.

Why It’s Important

- Mandatory by law (Motor Vehicles Act)

- Protects you from legal and financial liability

What It Does NOT Cover

- Your car repairs

- Theft of your car

- Natural calamity damage

Who Should Choose It

- Very old cars

- Cars with low resale value

- Owners looking for minimum legal compliance

Limitation

Cheap, but risky for your own car.

2. Comprehensive Car Insurance

What It Is

This is the most popular and recommended type of car insurance.

It includes:

- Third-party coverage

- Own-damage coverage

What It Covers

- Accidents

- Theft

- Fire

- Floods, cyclones, earthquakes

- Vandalism

- Damage during transit

Why Most Owners Choose It

- Complete protection

- Peace of mind

- Better resale confidence

Who Should Choose It

- New car owners

- Cars under loan

- Cars under 7–8 years old

This is the safest and most balanced option for most Indian drivers.

👉 Related read:

How Car Insurance Works in India – Simple Guide

3. Standalone Own-Damage Insurance

What It Is

This covers only damage to your own car.

You must already have:

- An active third-party insurance policy

Why It Exists

After 2018, IRDAI allowed buyers to:

- Choose third-party from one insurer

- Choose own-damage from another

Who Should Consider It

- Buyers who want flexibility

- Owners who want to optimise premium

- Those comparing insurers aggressively

This option suits experienced, informed buyers.

Add-On Covers (Optional but Important)

Add-ons increase premium—but can save money during claims.

Common Add-On Covers Explained

Zero Depreciation Cover

- No depreciation deduction on parts

- Best for new cars

- Highly recommended

Engine Protection Cover

- Covers engine damage due to water ingress

- Useful in flood-prone areas

Roadside Assistance

- Towing, battery jump-start, flat tyre help

Return to Invoice

- Pays original invoice value if car is total loss

- Useful in first 2–3 years

Add-ons are optional.

Choose based on usage, not fear.

👉 Helpful guide:

What Is Zero Depreciation Car Insurance – Benefits & Drawbacks

What Is NOT Covered (Policy Exclusions)

Every policy has exclusions. Common ones include:

- Drunk driving

- Driving without valid licence

- Wear and tear

- Mechanical failure

- Consequential damage

Reading exclusions avoids claim shock later.

IDV (Insured Declared Value) – Why It Matters

IDV is the maximum amount insurer pays if your car is stolen or totalled.

Key points:

- Higher IDV = higher premium

- Lower IDV = lower payout

- Correct IDV = market value

Never blindly choose highest or lowest IDV.

Myths vs Reality: Car Insurance in India

| Myth | Reality |

|---|---|

| Cheapest insurance is best | Coverage matters more |

| Dealer insurance is safest | Often most expensive |

| Insurance covers everything | Exclusions exist |

| Small claims don’t matter | They kill NCB |

| Online insurance is risky | Fully legal & regulated |

Common Mistakes Car Owners Make

❌ Buying insurance without comparison

❌ Choosing add-ons blindly

❌ Ignoring policy exclusions

❌ Claiming small repairs unnecessarily

❌ Forgetting No Claim Bonus

These mistakes increase premiums year after year.

👉 Learn how to reduce premium:

Save Money on Car Insurance – Indian Guide

How to Choose the Right Type of Car Insurance

Ask yourself:

- How old is my car?

- Can I afford repair costs myself?

- Is my area flood-prone?

- Is my car under loan?

Simple Recommendation

- New car: Comprehensive + zero depreciation

- Mid-age car: Comprehensive with selective add-ons

- Very old car: Third-party only

FAQs (Frequently Asked Questions)

1. Is third-party insurance enough?

Legally yes, practically no for most cars.

2. Is comprehensive insurance mandatory?

No, but highly recommended.

3. Can I change insurance type at renewal?

Yes, freely.

4. Are add-ons compulsory?

No, they are optional.

5. Does insurance price reduce as car ages?

Yes, if IDV and add-ons are optimised.

6. Can I buy insurance without dealer?

Yes, completely legal.

7. What’s the biggest insurance mistake?

Buying without understanding coverage.

Final Thoughts: Insurance Is Boring—But Ignoring It Is Expensive

Car insurance isn’t exciting.

But choosing the wrong type can cost you years of overpayment or one bad claim experience.

Once you understand:

- Types

- Coverage

- Limitations

Insurance stops being confusing—and starts working for you.

Strong CTA 🚗🛡️

👉 Bookmark this guide for renewal time

👉 Share it with a new car owner

👉 Explore more honest, India-first insurance guides on Car Insight Hub

Because smart insurance isn’t about paying less—

it’s about being protected correctly.

From my own personal experience

“I’ve personally noticed this while using my own car regularly in heavy city traffic. There was a time when I delayed a basic service by a few thousand kilometres, assuming it wouldn’t make much difference. Within weeks, the engine felt slightly rough and fuel efficiency dropped more than expected. A similar situation happened with a friend’s car as well, which clearly shows how small maintenance delays can impact long-term performance.”

References

- Society of Indian Automobile Manufacturers (SIAM)

- NITI Aayog Mobility Reports

- Economic Times Auto

- Government of India EV Portal (e-Amrit)

- Investopedia – Automobile Industry

Disclaimer: This article is published for general informational purposes based on research, observations, and owner experiences. It should not be considered professional, technical, or legal advice. Vehicle specifications, costs, and procedures may vary by model, location, and time. Readers are advised to verify details with official sources or qualified professionals before making decisions.