Introduction

If you own a car in India, you’ve probably heard the term “No Claim Bonus” while renewing your insurance. Most people know it helps reduce premium, but very few truly understand how it works, when it gets cancelled, and how to protect it.

In 2025, with rising insurance premiums and increasing repair costs, understanding NCB can save you a significant amount of money every year. For careful drivers, it’s actually one of the biggest financial advantages in car insurance.

This guide explains NCB in simple terms — no complicated insurance jargon — so you can make smarter decisions during renewal or claim situations.

What is No Claim Bonus (NCB)?

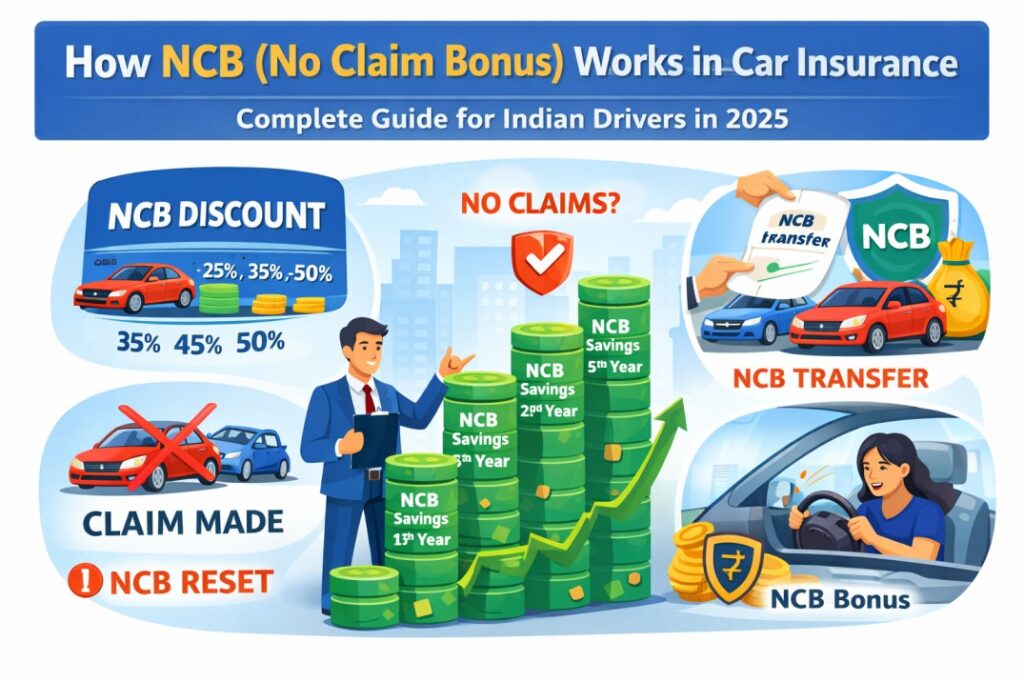

No Claim Bonus is a reward given by insurance companies when you do not make any claim during a policy year.

If you complete one full year without raising a claim, your insurer offers a discount on your own damage premium at renewal.

Important point:

NCB applies only to the “Own Damage” portion of comprehensive insurance. It does not apply to third-party insurance.

If you want to understand how insurance coverage is structured in India, read this beginner-friendly guide on how car insurance works in India simple guide for beginners.

How Much Discount Do You Get?

NCB increases every year if you continue without claims.

Here’s the standard structure in India:

- After 1 claim-free year: 20% discount

- After 2 consecutive years: 25%

- After 3 consecutive years: 35%

- After 4 consecutive years: 45%

- After 5 consecutive years: 50% (maximum)

50% is the highest NCB you can accumulate.

Example:

If your own damage premium is ₹10,000 and you have 50% NCB, you pay only ₹5,000 (before taxes and add-ons).

That’s a major saving.

Real-Life Example: Why NCB Matters

Let’s say two drivers buy the same car.

Driver A makes small claims every year for minor scratches.

Driver B avoids small claims and pays for minor repairs out of pocket.

After 5 years:

Driver B reaches 50% NCB and saves thousands every renewal.

Driver A stays at 0% because claims reset the bonus.

Small claims today can cost you big discounts tomorrow.

What Happens If You Make a Claim?

If you raise even one claim during the policy period, your NCB resets to 0% at renewal.

It doesn’t matter if:

- The claim amount was small

- The damage was minor

- You were not at fault

One claim = NCB reset.

This is why many experts advise avoiding claims for small repairs unless the repair cost is high.

What is NCB Protection Add-on?

In 2025, many insurance companies offer “NCB Protection Cover” as an add-on.

This allows you to:

- Make 1 or 2 claims in a year

- Without losing your accumulated NCB

It slightly increases premium but protects long-term savings.

Before buying it, compare costs carefully. Sometimes the add-on cost may not justify the benefit.

If you are evaluating different policies, you may also want to explore third-party vs comprehensive car insurance which is better to understand coverage differences.

Is NCB Linked to Car or Owner?

This is very important.

NCB belongs to the car owner, not the vehicle.

If you sell your car:

- Your NCB stays with you.

- You can transfer it to your new car.

However, you must request an NCB certificate from your previous insurer.

Many people lose their bonus simply because they don’t claim the certificate during sale.

Can You Transfer NCB to Another Insurance Company?

Yes.

If you switch insurers, your accumulated NCB can be transferred.

You need:

- Renewal notice

- Previous policy copy

- NCB confirmation

Insurance companies verify this information during policy issuance.

Switching insurers does not cancel your bonus — as long as there was no claim.

What Happens If Policy Lapses?

If your policy expires and is not renewed within 90 days, you may lose your NCB benefits.

Grace period matters.

Always renew on time to protect accumulated discounts.

Should You Avoid Claims to Save NCB?

Not always.

Here’s how to decide:

If repair cost is ₹3,000 and your NCB benefit next year is ₹8,000 — it may be better to pay yourself.

If repair cost is ₹40,000 — claiming insurance makes sense even if NCB resets.

Think long-term.

Also remember, insurance exists for financial protection. Don’t avoid legitimate claims out of fear.

For better clarity on claim procedures, you can refer to how to claim car insurance after an accident before making decisions.

How NCB Impacts Long-Term Savings

Let’s calculate roughly:

Assume:

Own damage premium = ₹12,000

50% NCB = ₹6,000 saved yearly

Over 5 years:

You save around ₹30,000 (excluding tax impact).

That’s not a small amount.

In 2025, as repair costs rise due to advanced car technology, insurance premiums are also increasing. NCB becomes even more valuable.

Common Myths About NCB

Myth 1: Small claim won’t affect NCB

Truth: Any claim resets it unless you have NCB protection add-on.

Myth 2: NCB applies on total premium

Truth: It applies only on own damage component.

Myth 3: NCB cannot be transferred

Truth: It can be transferred to a new insurer or new car.

Myth 4: Third-party insurance gives NCB

Truth: NCB applies only to comprehensive policies.

Tips to Maximise Your NCB in 2025

- Avoid claiming for minor scratches.

- Drive carefully to reduce accident risk.

- Install dashcam for dispute clarity.

- Compare insurance options every year.

- Consider NCB protection add-on if you have high NCB percentage.

If you’re planning renewal soon, reviewing best car insurance companies in India 2025 comprehensive reviews buying guide can help you compare policy benefits wisely.

Final Thoughts

No Claim Bonus is one of the most powerful money-saving features in Indian car insurance.

It rewards responsible driving and smart financial decisions. But many drivers lose it due to lack of awareness.

Before filing a claim, calculate the impact. Before switching insurers, secure your NCB certificate. Before renewal, compare options.

In 2025, when every rupee matters, understanding NCB properly can help you save thousands over time.

Insurance is not just about protection — it’s also about planning smartly.

Drive safely. Claim wisely. Protect your bonus.

From my own personal experience

“I’ve personally noticed this while using my own car regularly in heavy city traffic. There was a time when I delayed a basic service by a few thousand kilometres, assuming it wouldn’t make much difference. Within weeks, the engine felt slightly rough and fuel efficiency dropped more than expected. A similar situation happened with a friend’s car as well, which clearly shows how small maintenance delays can impact long-term performance.”

References

- Society of Indian Automobile Manufacturers (SIAM)

- NITI Aayog Mobility Reports

- Economic Times Auto

- Government of India EV Portal (e-Amrit)

- Investopedia – Automobile Industry

Disclaimer: This article is published for general informational purposes based on research, observations, and owner experiences. It should not be considered professional, technical, or legal advice. Vehicle specifications, costs, and procedures may vary by model, location, and time. Readers are advised to verify details with official sources or qualified professionals before making decisions.